Introduction

In our increasingly digital economy, the ability to process online transactions efficiently has become essential for businesses of all sizes. Payment aggregators serve as critical intermediaries that simplify the complex ecosystem of digital payments. This guide explores how payment aggregators function, their advantages, potential challenges, and the regulatory environment they operate within.

Understanding Payment Aggregators

A payment aggregator functions as a third-party service provider that enables digital payment processing between customers and merchants. These platforms allow businesses to accept various payment methods including credit and debit cards, UPI (Unified Payments Interface), digital wallets, bank transfers, EMIs, and e-mandates.

In regulated markets like India, payment aggregators must obtain proper licensing from regulatory authorities such as the Reserve Bank of India (RBI). This licensing ensures adherence to security protocols and compliance standards designed to protect all parties involved in transactions.

The Payment Aggregation Process

The way payment aggregators operate involves several interconnected steps:

- Merchant Registration: Businesses must first establish a merchant account with the payment aggregator. The aggregator maintains a nodal account with a banking partner where all customer transactions are processed.

- Payment Initiation: When customers reach the payment stage, they select their preferred payment method and enter their details. The payment aggregator immediately tokenizes this sensitive information and conducts preliminary fraud screening.

- Background Transaction Processing: The aggregator forwards transaction information to their banking partner, which then routes this data to the appropriate card network or payment processor.

- Security Verification: The card network or payment system performs fraud detection analysis based on the customer’s transaction history and pattern recognition algorithms.

- Customer Bank Authorization: The customer’s banking institution verifies available funds and account details, then sends an approval or denial message back through the same channels.

- Fund Transfer Request: Upon approval, the aggregator’s banking partner requests the transfer of funds from the customer’s financial institution to the nodal account.

- Settlement Process: Payment aggregators typically process batch settlements to merchant accounts, though some offer premium instant settlement options for additional fees.

Categories of Payment Aggregators

Payment aggregators generally fall into two main categories:

Bank-Operated Aggregators

- Operated directly by financial institutions

- May require more extensive integration processes

- Often have higher setup and operational costs

- May lack advanced analytics and merchant tools

- Typically have established infrastructure and compliance frameworks

Third-Party Aggregators

- Operated by specialized fintech companies

- Require regulatory authorization to operate

- Generally offer more accessible integration options

- Typically provide more competitive pricing structures

- Often include additional features like analytics dashboards

- May offer more flexible solutions for smaller businesses and startups

Key Benefits of Payment Aggregators

Enhanced Merchant Capabilities

Payment aggregators enable businesses to create sub-merchant accounts, allowing platforms to manage payments on behalf of partner businesses. This feature is particularly valuable for marketplace business models and multi-vendor platforms.

Advanced Security Infrastructure

Payment aggregators implement robust security measures including:

- Enterprise-grade infrastructure security

- Minimized storage of sensitive data

- Strong encryption protocols

- Tokenization of payment information

- Compliance with industry standards like PCI-DSS

Sophisticated Fraud Prevention

Using advanced machine learning algorithms, payment aggregators analyze transaction patterns to identify potential fraud. These systems continuously improve by learning from both legitimate transactions and previously detected fraudulent activities.

Payment Method Diversity

Integrating with a payment aggregator allows businesses to offer customers numerous payment options, including:

- Credit and debit cards

- Internet banking services

- UPI transactions

- EMI payment plans

- Digital wallets

- Buy Now Pay Later (BNPL) options

- Recurring payment setups

Flexible Settlement Options

Payment aggregators often provide various settlement timeframes to accommodate different business needs:

- Instant settlement (for a premium fee)

- Same-day settlement options

- Standard settlement periods

- Settlements during non-banking hours and holidays

Optimized Checkout Experience

Payment aggregators invest significantly in creating intuitive, frictionless checkout experiences that minimize abandonment rates and maximize conversion.

Dedicated Support Systems

Most established payment aggregators maintain specialized customer support teams trained to address technical issues, payment disputes, and merchant concerns.

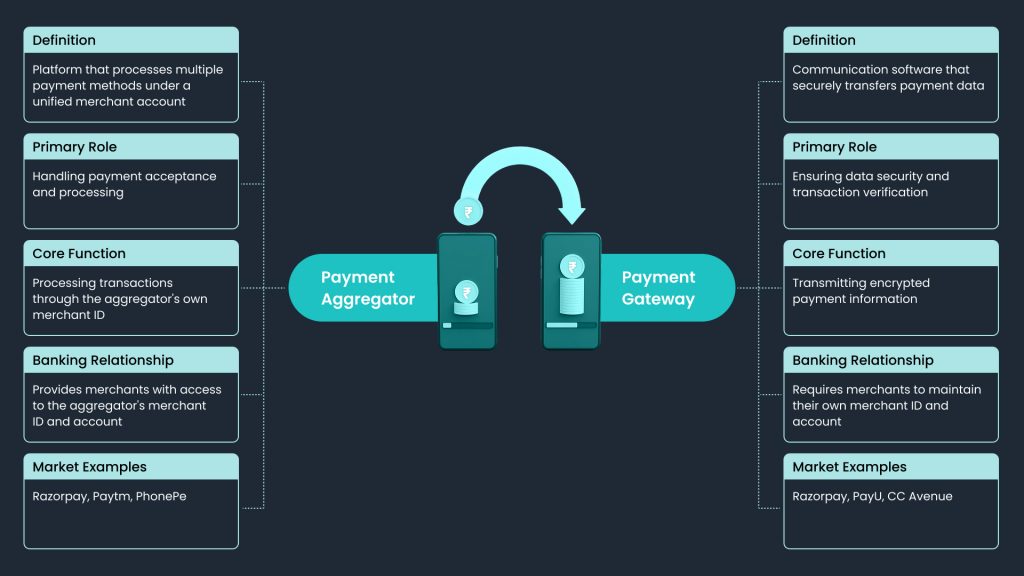

Payment Aggregators vs. Payment Gateways

While often confused, payment aggregators and payment gateways serve different functions:

Conclusion

Payment aggregators play an instrumental role in modernizing digital commerce by simplifying the acceptance of online payments. By offering a consolidated solution for managing diverse payment methods, these services enable businesses of all sizes to provide customers with secure, efficient payment experiences while streamlining back-end financial operations.

Common Questions

Q: What are prominent payment aggregators in the Indian market?

A: Leading payment aggregators in India include Razorpay, Paytm, and PhonePe.

Q: What licensing requirements apply to payment aggregators?

A: In India, payment aggregators must obtain proper licensing from the RBI, which includes meeting specific financial requirements such as maintaining a minimum net worth of INR 15 crore (initially) and INR 25 crore by later deadlines.

Q: How do payment aggregators generate revenue?

A: Payment aggregators typically earn through transaction fees, setup charges, monthly service fees, and premium services like instant settlement.

Q: What risks do payment aggregators face?

A: Payment aggregators must manage risks including cyberattacks, fraudulent transactions, and compliance breaches, requiring substantial investment in security infrastructure.

Q: Are UPI payments supported by most payment aggregators?

A: Yes, virtually all payment aggregators operating in India support UPI payments due to its widespread adoption.

Q: How many authorized payment aggregators operate in India?

A: Recent data indicates approximately 32 payment aggregators have received in-principle authorization from the RBI, with additional applications under review.

Q: What is a nodal account in payment aggregation?

A: A nodal account is a specialized bank account maintained by payment aggregators where customer payments are temporarily held before being distributed to merchant accounts, subject to regulatory oversight.

Q: Do payment aggregators offer business intelligence tools?

A: Many third-party payment aggregators provide analytics dashboards and reporting features that help businesses gain insights into their transaction patterns and payment trends.

Leave a Reply