In the digital-first era today, Know Your Customer (KYC) is the foundation of trust between companies and customers. Whether one is opening a new bank account, investing in mutual funds, taking a loan, or enrolling on a fintech platform, KYC verifies that the individual behind the transaction is authentic.

But as with all security procedures, fraudsters are never far behind. In the past few years, frauds in KYC have been increasing exponentially, taking advantage of technological loopholes as well as human weak points.

Consider this case in point:

A young woman was browsing the internet for a new credit card and the best deals on offer. Browsing social media, she came across what appeared to be an authentic link from a bank. She clicked on it, filled in her personal information, and without knowing it, continued authorizing every request that appeared. In minutes, the criminals had access to her full set of sensitive data—identity documents, phone information, even bank details. Not only was her data hijacked now, but the scammers started blackmailing her as well, threatening to abuse the details if she did not pay them off.

Alas, this is not an isolated tale. Thousands of similar scams occur every day and leave the victims financially exposed and emotionally battered. For consumers, the scams can translate into stolen identities, depleted bank accounts, or unwittingly being associated with criminal activities. For corporations, the scams equate to regulatory penalties, reputational losses, and loss of capital.

So how do KYC frauds actually occur? And more importantly, what can you do to protect yourself? Let’s dive in.

What is KYC Fraud Actually?

KYC fraud is any kind of fraudulent act in which the KYC process is manipulated or abused by criminals for illegal purposes. Basically, fraudsters deceive people, financial institutions, or service providers into accepting forged, stolen, or manipulated identity documents.

The objective may be varied based on the scam:

- Opening accounts in fraudulent or stolen identities.

- Opening loans and vanishing with forged documents.

- Using stolen credentials to hijack money laundering.

- Tampering with the onboarding flow of mobile apps to abuse freebies or cashbacks.

In essence, KYC fraud is about breaching trust at the very initial step of a financial relationship.

How Do KYC Frauds Occur?

While every case may look different, most KYC frauds fall into certain recognizable patterns. Understanding these methods is the first step in protecting yourself.

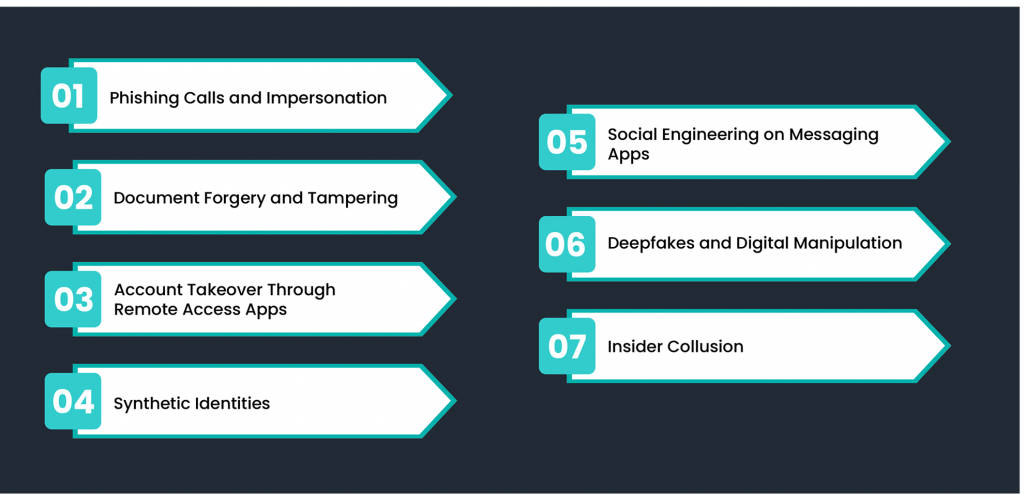

1. Phishing Calls and Impersonation

This is perhaps the most frequent technique. You get a call from someone who identifies himself as an employee of your bank, your payment wallet, or even the Reserve Bank of India. The caller informs you that your KYC is up for renewal, or your account gets blocked otherwise if you don’t do something immediately.

They then request you to give them sensitive information—such as Aadhaar numbers, PAN information, OTPs, or even pictures of your ID cards. At times, they may send you a fake link in the name of an official update form. These details, once given, are exploited to duplicate your identity.

Real Example: In India, thousands of digital wallet customers were victims of fraudsters posing as “KYC update executives.” They were tricked into sharing OTPs, enabling fraudsters to withdraw money in an instant.

2. Document Forgery and Tampering

The fraudsters have a tendency to use forged PAN cards, Aadhaar cards, passports, or voter IDs. These can be produced with advanced design software or manipulated copies of authentic documents.

For example, a con artist might steal a valid ID card, alter the photo, and reprint it using high-end equipment. To the naked eye—or even to some traditional onboarding systems—it would appear valid.

In loan fraud, falsified salary slips and phony addresses are also provided along with fake IDs, which complicate detection for banks.

3. Account Takeover Through Remote Access Apps

Another emerging trend is where scammers trick victims into downloading remote access software like AnyDesk or TeamViewer as part of “KYC verification.” Once downloaded, scammers have access to the victim’s smartphone, including SMS inboxes, bank apps, and saved documents.

This is a two-whammy: not only is the victim’s KYC information compromised, but also his/her bank account can be sucked dry in real-time.

4. Synthetic Identities

This is more advanced fraud. Criminals put together shreds of genuine identities—someone’s Aadhaar number and someone else’s PAN card information, for instance—to form a synthetic identity.

This synthetic identity is convincing enough to get through simple verification processes. Fraudsters then utilize these “ghost identities” to open accounts, run money laundering operations, or get credit lines that they have no intention of repaying.

5. Social Engineering on Messaging Apps

Phishers have taken their playgrounds to WhatsApp, Telegram, and LinkedIn as well. Victims are being contacted with a job offer, investment opportunity, or renewal of KYC. A fake PDF or link is sent, which extracts sensitive details or loads malware.

Since the message appears to come from a personal or professional acquaintance, victims tend to drop their guard.

6. Deepfakes and Digital Manipulation

With the use of AI-enabled tools, cybercriminals can now produce deepfake videos to impersonate a person making video KYC calls. Suppose a fraudster accesses your stolen picture to create a real-time video that replicates your face and voice.

Though still nascent, this type of fraud has been a massive threat to banks and fintech organizations that use video-based verification.

7. Insider Collusion

In a few sad instances, KYC fraud is facilitated by insiders—financial institution employees who fraudulently sign off on forged documents for bribes. Although infrequent, these cases illustrate why it is necessary to have several layers of verification in place.

Why KYC Frauds Are Hazardous

The implications of KYC fraud extend far beyond direct financial loss.

- Identity Theft: Your identity stolen from you could be used to create shell companies or be involved in criminal activities, and you’d be left struggling to clear your name.

- Financial Loss: The fraudsters can obtain loans in your name, which means debt collectors knocking on your door.

- Reputational Damage: For companies, having fraudulent customers onboard erodes credibility and even exposes them to regulatory penalties.

- Legal Issues: If you’re associated with illegal things such as money laundering, your name could take years to be cleared.

Tips to Prevent Getting Scammed

The good news? With awareness and precautions, most KYC frauds can be avoided. Here’s a comprehensive checklist:

1. Never Share Personal Details Over Calls

No legitimate bank or financial institution will ever ask for your Aadhaar number, PAN details, OTPs, or net banking credentials over a phone call. Treat unsolicited KYC calls as red flags.

2. Verify the Source Before Acting

If you are receiving an SMS or email notification for KYC renewal, verify if it is from a reliable domain or verified number. In case you are unsure, log in to your bank’s app or website directly rather than clicking on common links.

3. Be cautious of Remote Access Apps

Do not install apps such as AnyDesk or TeamViewer on the instructions of unknown callers. These applications provide remote access to your device to strangers.

4. Verify Documents Thoroughly

For businesses, invest in document verification tools that can detect forged IDs, altered fonts, or mismatched holograms. For individuals, be cautious if you’re asked to hand over original documents to anyone other than an authorized official.

5. Enable Multi-Factor Authentication

Even if fraudsters get hold of your credentials, multi-factor authentication (such as OTPs or biometric checks) adds a strong protective layer.

6. Update Your KYC Only Through Official Channels

Banks and supervised institutions offer safe portals, applications, and physical offices for KYC updates. Refrain from shortcuts or third-party representatives except as officially assigned.

7. Learn About Emerging Fraud Trends

Be current with news notifications, RBI notifications, and banking awareness drives. The more you learn about changing fraud techniques, the less susceptible you will become.

8. Check Your Financial Accounts Periodically

Monitor your bank accounts and credit reports regularly. Any unknown loan, payment, or inquiry should be pursued urgently.

9. Report Suspicious Activity Without Delay

In case you find your KYC information has been abused, alert your bank and lodge a complaint with cybercrime agencies. Prompt action will avert further loss.

How Businesses Can Strengthen KYC Defenses

While people need to be careful, organizations have an even greater onus. Companies who onboard customers with insufficient checks risk not just financial loss but regulatory fines.

Some of the best practices for companies:

- Embrace AI-Powered Verification: Utilize software that can identify deepfakes, fake IDs, and synthetic identities.

- Layered Security Strategy: Combine document verification, biometric screening, and CPV (Contact Point Verification) where applicable.

- Real-Time Fraud Detection: Always monitor customer activity for fraudulent behavior.

- Employee Education: Train employees to detect fraud indicators and follow procedures.

- Regular Audits: Regularly audit KYC procedures to spot gaps.

The Road Ahead

Financial services will move increasingly online, and fraudsters will adapt their playbook accordingly. The emergence of AI-generated forgeries and deepfakes indicates that tomorrow’s cons will be even more difficult to spot to the naked eye.

But that does not mean the war is lost. Greater awareness among people and more intelligent verification processes for companies can prevent KYC fraud to a large extent.

In essence, KYC is not only a regulatory necessity; it is the pillar of secure financial transactions. Yet misused, it becomes an even more potent weapon in the hands of scammers. From spoof calls to synthetic identities and deepfakes, the tools are aplenty.

The key is vigilance, education, and multi-layered security controls. As individuals, we need to learn to say no to unwanted requests and employ only sanctioned channels. As enterprises, we need to adopt sophisticated verification tools and ongoing monitoring.

In a day and age where information is as precious as cash, safeguarding your identity is not a choice—it is a necessity. The next time you receive a call asking you for a KYC request, hold on, authenticate, and recall: trust, but first verify.

Leave a Reply