Compliance in banking is no longer just about avoiding penalties. In today’s environment, it has quietly become a condition for survival.

Indian banks are operating in a pressure cooker. Digital adoption has exploded. Financial products are more complex. Fraud has become faster, smarter, and more organised. At the same time, regulators expect tighter controls, better reporting, and stronger accountability — not just on paper, but in practice.

What makes this moment different is that customers now feel compliance failures directly. A fraud incident, a data leak, or a frozen account doesn’t just attract regulatory attention — it erodes trust. And once trust breaks, customers don’t wait for annual reports. They leave.

This is why many banks are shifting from reactive compliance to a checklist-driven, risk-first approach — one that ensures nothing critical is missed as operations scale.

Below is a practical, India-specific banking compliance checklist — grounded in regulation, shaped by technology, and aligned with how banks actually function today.

The Regulatory Landscape Indian Banks Operate In

Before getting into the checklist, it’s important to understand the ecosystem banks operate within.

Indian banking compliance is governed by multiple authorities, each playing a distinct role:

- The Reserve Bank of India (RBI) sets the core framework for KYC, AML, cybersecurity, and operational risk.

- FIU-IND oversees reporting related to suspicious and high-value transactions.

- CERT-In defines obligations around cyber incident reporting.

- Data protection obligations are now shaped by the Digital Personal Data Protection (DPDP) framework, which is moving into active enforcement.

This layered oversight means compliance is not about one regulation — it’s about coordination across systems, teams, and timelines.

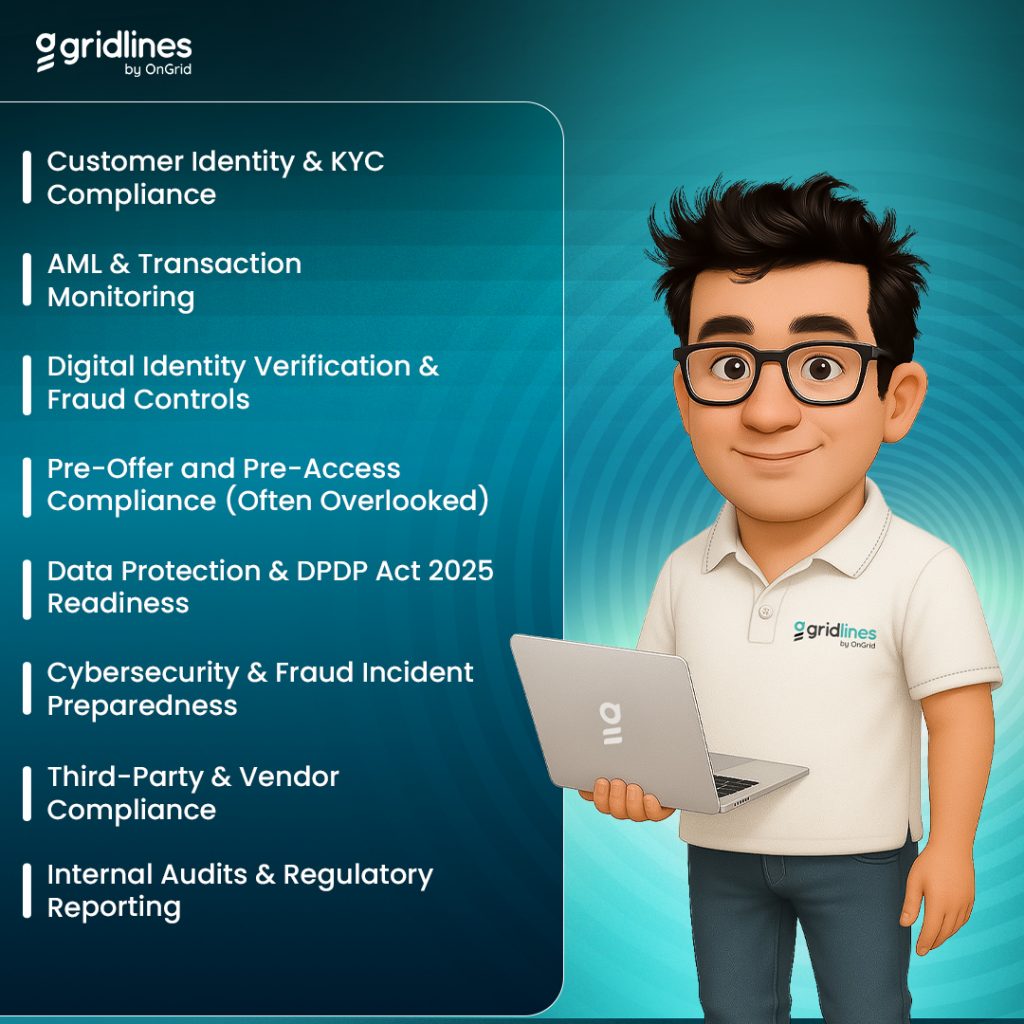

The Core Banking Compliance Checklist

1. Customer Identity & KYC Compliance

At the heart of banking compliance lies identity.

Banks must ensure that every customer is who they claim to be — not just at onboarding, but throughout the relationship. This involves:

- National ID verification using officially recognised identity documents

- Risk-based KYC, where higher-risk customers undergo enhanced scrutiny

- Periodic KYC updates to ensure records remain current

With digital onboarding now the norm, identity checks are often the first line of defence against mule accounts, impersonation, and downstream fraud. Weak identity foundations almost always show up later as compliance failures.

2. AML & Transaction Monitoring

Anti-Money Laundering compliance is no longer limited to ticking reporting boxes.

Banks are expected to:

- Monitor transactions continuously

- Detect unusual patterns across accounts and channels

- File Suspicious Transaction Reports (STRs) and Cash Transaction Reports (CTRs) within defined timelines

- Identify beneficial ownership behind accounts and entities

In India’s real-time payment environment, where money moves instantly and at scale, delayed detection is ineffective detection. AML systems must work in near real time — or risk becoming irrelevant.

3. Digital Identity Verification & Fraud Controls

Fraud today rarely looks obvious.

Identity misuse is increasingly assisted by technology — fake documents, proxy onboarding, and impersonation across digital channels. This has pushed banks to move beyond basic document checks.

Modern compliance requires:

- Verifying that the person presenting an identity is the rightful owner

- Detecting inconsistencies across identity, device, and behavioural signals

- Identifying synthetic or recycled identities early

Strong digital identity verification helps banks stop fraud before it becomes a transaction problem, rather than chasing losses after the fact.

4. Pre-Offer and Pre-Access Compliance (Often Overlooked)

One of the most common gaps in banking compliance appears before exposure, not after.

Banks often perform detailed checks only once:

- An account is activated

- A credit line is issued

- Access to systems is granted

Increasingly, leading banks are introducing pre-offer , ensuring that identity and risk checks happen before:

- High-value accounts are approved

- Credit limits are extended

- Employees, vendors, or partners gain system access

This shift reduces downstream remediation and protects institutions from avoidable risk.

5. Data Protection & DPDP Act 2025 Readiness

Compliance is no longer just about collecting data — it’s about handling it responsibly.

Under the DPDP framework, banks must ensure:

- Clear consent for data collection

- Purpose limitation — collecting only what is necessary

- Defined retention and deletion policies

- Preparedness for breach response and reporting

The direction is clear: banks are expected to verify trust without stockpiling personal data. Systems that minimise storage while still enabling strong verification are becoming the safer long-term choice.

6. Cybersecurity & Fraud Incident Preparedness

Banks are prime targets for cybercrime.

Compliance today includes:

- Defined cyber incident response plans

- Adherence to CERT-In reporting timelines

- Employee access controls and monitoring

- Regular security testing and audits

Cyber incidents are no longer hypothetical. Preparedness determines whether an incident becomes a contained event — or a reputational crisis.

7. Third-Party & Vendor Compliance

Modern banking runs on partnerships — fintechs, payment processors, verification providers, and service vendors.

Banks must ensure:

- Proper due diligence before onboarding partners

- Contractual clarity on data handling and compliance responsibilities

- Ongoing monitoring and audits

When compliance fails at a vendor level, accountability still rests with the bank. Third-party risk is no longer indirect risk — it is direct exposure.

8. Internal Audits & Regulatory Reporting

No compliance framework is complete without strong internal oversight.

Banks must maintain:

- Audit trails for KYC, verification, and transactions

- Clear documentation for regulatory inspections

- Regular internal audits to identify gaps before regulators do

Audits are not about fault-finding. They are about resilience — ensuring systems hold up under scrutiny.

Common Compliance Gaps Seen in Indian Banks

Despite best intentions, many banks struggle with:

- Manual, fragmented compliance processes

- Legacy systems that don’t integrate well

- Siloed data across teams

- Compliance triggered only after incidents

These gaps often widen as transaction volumes and digital channels grow.

How Technology Is Reshaping Banking Compliance

Technology is no longer optional in compliance — it is the only way to operate at scale.

API-led verification, real-time monitoring, and automated reporting allow banks to:

- Reduce manual effort

- Improve accuracy

- Respond faster to risk

The shift is from after-the-fact checks to continuous assurance.

Building a Future-Ready Compliance Framework

Banks that lead in compliance share a few traits:

- They prioritise risk-based controls

- They automate high-volume processes

- They reserve human judgement for complex decisions

- They treat compliance as trust infrastructure, not overhead

Conclusion: Compliance as a Competitive Advantage

Indian banks don’t lose customers because of regulation.

They lose customers when trust breaks.

A strong compliance checklist doesn’t slow growth — it enables safe growth. As banking becomes more digital, more connected, and more exposed, compliance will increasingly define which institutions scale with confidence and which struggle under scrutiny.

In the end, banking compliance is not just about following rules.

It’s about earning — and keeping — trust.

Leave a Reply