Identity verification plays a vital role in shaping the future of financial services. With the need for secure and seamless onboarding, the KYC (Know Your Customer) process has evolved from traditional paper-based systems to more sophisticated, digital-first solutions. Among these, CKYC vs. eKYC has become a central discussion point in understanding how these frameworks impact the broader financial ecosystem.

Let’s dive deep into what these two systems are, how they differ, and what role they play in enhancing financial inclusion, security, and efficiency.

Must read: Safeguarding Privacy in Aadhaar Card KYC: Risks, Solutions, and Best Practices

Understanding CKYC and eKYC

What is CKYC?

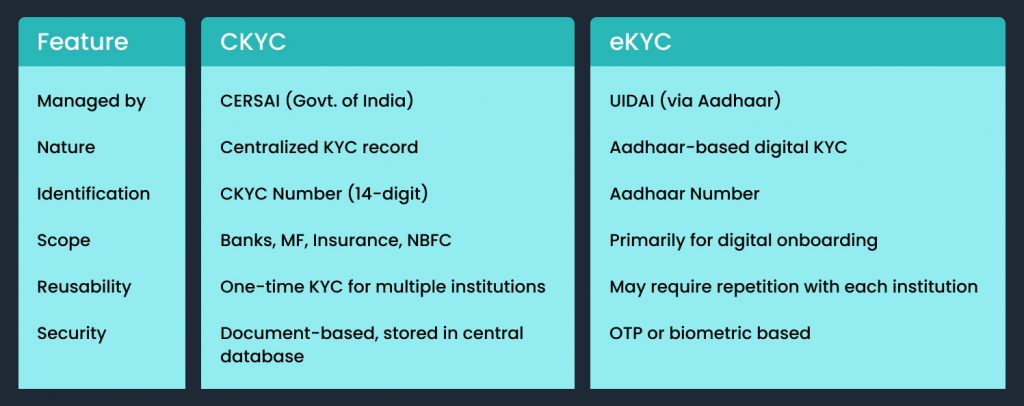

CKYC stands for Central Know Your Customer, a centralized repository of KYC records introduced by the Government of India. Managed by CERSAI (Central Registry of Securitisation Asset Reconstruction and Security Interest of India), CKYC aims to eliminate the need for multiple KYC submissions across financial institutions.

Once a customer completes CKYC, they receive a 14-digit CKYC number, which can be used across banks, insurance firms, mutual fund houses, and NBFCs. The idea is simple: One KYC for all financial services.

What is eKYC?

eKYC, or electronic Know Your Customer, is a digital method of verifying identity, primarily through Aadhaar-based authentication. It is an online, paperless system where customer identity and address can be verified using Aadhaar OTP or biometric verification. It is widely used for onboarding customers in real-time with minimal friction.

CKYC vs. eKYC: Core Differences

The Role of CKYC and eKYC in the Financial Ecosystem

1. Accelerating Financial Inclusion

Both CKYC and eKYC play a monumental role in improving access to financial services. In a country like India, where millions are still unbanked, the ability to authenticate identity quickly and securely is a game-changer. eKYC allows people in remote areas to open bank accounts or apply for loans using just a mobile phone and Aadhaar. CKYC, on the other hand, ensures that once KYC is completed, it doesn’t need to be redone for future financial needs.

2. Reducing Duplication and Operational Costs

The traditional KYC process involved physical documentation, manual verification, and often, redundant efforts for every new financial service a customer opted for. With CKYC, the duplication of KYC across multiple institutions is eliminated. eKYC further reduces operational costs by making the process automated, instantaneous, and paperless.

3. Enabling Real-Time Customer Onboarding

The speed of eKYC is unparalleled. With OTP-based or biometric verification, financial institutions can onboard customers in minutes. This agility is essential for fintechs, digital banks, and platforms offering real-time services. While CKYC is not instantaneous, it supports a smoother onboarding journey by allowing reuse of verified KYC data.

4. Ensuring Compliance and Regulatory Adherence

Regulators demand stringent customer verification to prevent fraud, money laundering, and identity theft. CKYC and eKYC help institutions meet compliance requirements efficiently. The centralized nature of CKYC adds an extra layer of credibility and traceability, while eKYC ensures real-time, government-backed verification.

5. Building Trust in the Financial Ecosystem

Both CKYC and eKYC enhance trust between customers and financial institutions. A verified customer identity reduces the risk of impersonation or fraud. In turn, this helps in building a more transparent, secure, and inclusive financial landscape.

The Future: Integration and Innovation

The future of KYC lies in hybrid systems that combine the strengths of CKYC and eKYC. Innovations like Video KYC are already making waves by providing an extra layer of verification without physical meetings. As regulators evolve, we can expect even more seamless, AI-powered, and privacy-centric identity verification tools.

How Gridlines is Shaping the Future with eKYC and Video KYC

In this rapidly evolving landscape, companies like Gridlines are redefining what modern KYC should look like. Gridlines offers powerful features that streamline the entire identity verification process for businesses and customers alike.

✅ eKYC with Gridlines

- Instantly verify customer identity using Aadhaar-based eKYC.

- Fast, secure, and compliant with regulatory standards.

- Perfect for digital-first institutions that want to scale rapidly.

🎥 Video KYC with Gridlines

- Conduct secure and guided Video KYC sessions in real-time.

- AI-driven facial recognition and document validation.

- Fully compliant with RBI/SEBI norms.

- Ideal for onboarding customers remotely without compromising on compliance or trust.

Whether you’re a bank, fintech startup, or an NBFC, Gridlines empowers you with plug-and-play solutions that are fast, secure, and future-ready.

Conclusion

The debate of CKYC vs. eKYC is not about which is better, but about how both can coexist to build a more robust, inclusive, and efficient financial ecosystem. CKYC offers permanence and centralized verification, while eKYC brings agility and convenience. Together, they enable financial institutions to serve customers better, faster, and more securely.

As technology continues to advance, innovative platforms like Gridlines are taking this vision forward with next-gen solutions like eKYC and Video KYC, ensuring that onboarding is not just a regulatory checkbox—but a seamless, trusted experience.

FAQ’S

1. What is the difference between CKYC and eKYC?

CKYC is a centralized KYC system managed by CERSAI, while eKYC is an Aadhaar-based digital identity verification method managed by UIDAI. CKYC is reusable across multiple financial institutions, whereas eKYC is primarily used for quick digital onboarding.

2. Can I use my eKYC to complete CKYC?

Yes, in many cases, Aadhaar-based eKYC can be used to populate CKYC records. Once verified and uploaded, a CKYC number is issued for future use across institutions.

3. Is eKYC safe and secure for identity verification?

Yes, eKYC is governed by UIDAI and uses OTP or biometric-based verification. It’s designed to be secure, paperless, and compliant with privacy standards set by Indian regulations.

4. How do platforms like Gridlines improve the KYC process?

Gridlines offers plug-and-play solutions like eKYC and Video KYC to help financial institutions onboard customers faster, more securely, and in compliance with regulatory norms—without physical paperwork.

5. What makes Gridlines’ Video KYC different from others?

Gridlines uses AI-powered facial recognition, document validation, and liveness detection to conduct secure Video KYC sessions in real time. It’s fully compliant with RBI/SEBI guidelines and ideal for remote onboarding.

Leave a Reply