“You don’t need to rob a bank to launder money these days — you just need a naive customer and a smartphone.”

Money mule accounts are rapidly becoming a preferred weapon of choice for cybercriminals. As banks and NBFCs invest in sophisticated digital infrastructure, criminals adapt and exploit human loopholes instead — namely, unsuspecting or compromised account holders.

This blog aims to uncover what money mule accounts are, why their presence is spiking, and how financial institutions can take a proactive approach to detect and prevent them.

What Exactly Is a Money Mule Account?

A money mule is a person who transfers illegally obtained money on behalf of others. The mule might be willing, coerced, or unaware that they’re part of a criminal enterprise. The account used in such activity is termed a money mule account.

Imagine this: a college student responds to a work-from-home job listing. The “company” offers to pay a high commission for processing payments. The student agrees, shares bank account details, and soon starts receiving large deposits, which they are asked to transfer elsewhere. Unknowingly, they’ve become a money mule for a scam operation.

This “outsourced” laundering method is simple, scalable, and hard to trace — and that’s exactly why fraud networks love it.

Must Read: Money Mules Unveiled

Why the Sudden Surge in Money Mule Accounts?

Several interconnected trends have accelerated the rise of money mule networks in India and globally:

1. Explosion of Digital Banking & NBFC Services

With onboarding becoming fully digital, opening a bank or NBFC account can be completed in minutes. This convenience, while great for customers, can be exploited by fraudsters using fake, forged, or synthetic identities.

2. Increase in Cyber Fraud & Phishing

Scams like job frauds, investment scams, romance scams, and phishing attacks are rampant. Criminals use these methods to convince individuals to “lend” their bank accounts for seemingly legitimate reasons.

3. Pandemic-Induced Financial Vulnerability

Many people, especially gig workers and students, became financially vulnerable during the COVID-19 pandemic, making them easy targets for “get-rich-quick” mule recruitment.

4. Globalization of Crime Networks

Sophisticated international fraud networks need ways to move money without raising red flags. Enter mule accounts, which provide a local layer of obfuscation.

5. Regulatory Crackdown on Direct Laundering

As KYC norms tighten and crypto traceability improves, criminals are pivoting to indirect methods — mule accounts provide a human firewall to avoid direct exposure.

Common Red Flags: How to Identify a Potential Mule Account

Detecting a mule account isn’t always straightforward, but there are behavioural and transactional patterns that raise suspicion:

- Sudden increase in account activity after long periods of dormancy

- Frequent high-value credits followed by immediate withdrawals or transfers

- Round-number transactions with no clear purpose

- Discrepancies between customer profile and transaction type (e.g., a student account receiving large business payments)

- Shared KYC details or device fingerprints across multiple accounts

- Multiple accounts opened using similar documentation or addresses

These indicators, when detected early, can prevent large-scale losses and reputational damage.

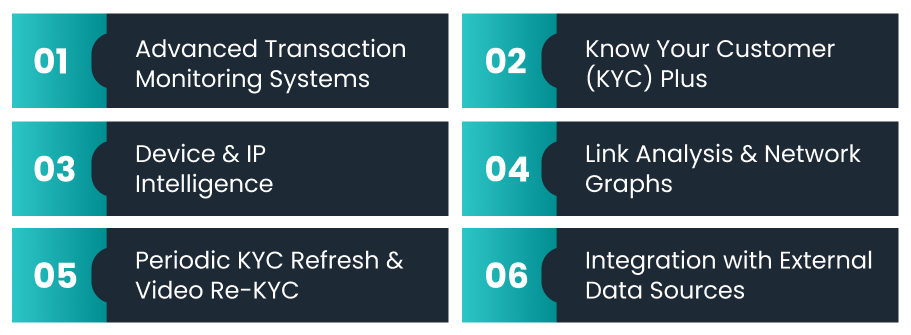

How Can Banks & NBFCs Detect Money Mule Accounts?

Let’s break down the key tools and techniques financial institutions can use:

1. Advanced Transaction Monitoring Systems

Leverage AI/ML-powered rule engines that flag anomalous patterns. These can include velocity checks (how fast money moves), round-figure transactions, and geolocation mismatches.

2. Know Your Customer (KYC) Plus

Beyond the basic KYC, implement dynamic profiling. This means updating risk scores based on evolving behavior and external risk indicators.

3. Device & IP Intelligence

Monitor for accounts accessed from risky geographies, TOR networks, or previously blacklisted IP addresses. Track if multiple accounts are logging in from the same device/browser fingerprint.

4. Link Analysis & Network Graphs

Use graph-based analytics to identify hidden relationships — like multiple accounts transacting with the same beneficiary or sharing KYC elements (like PAN, phone numbers, etc.).

5. Periodic KYC Refresh & Video Re-KYC

Trigger re-verification workflows for dormant accounts that suddenly become active. Video KYC can serve as a deterrent and a validation mechanism.

6. Integration with External Data Sources

Tap into government or third-party databases to verify employment history, criminal background, and court records. This can help flag high-risk individuals before account opening.

Platforms like OnGrid offer APIs for every business use case, including criminal checks, business verification, employment history checks, etc, via Gridlines, making onboarding safer and more reliable.

Case in Point: Synthetic IDs & Mule Rings

In 2023, Indian banks reported several large fraud rings where hundreds of mule accounts were opened using synthetic identities — a mix of real and fake information. These were then used to funnel fraud proceeds from crypto scams and UPI frauds across state lines.

Many of these accounts were dormant for months and suddenly became active, highlighting the need for real-time behavioral analytics alongside traditional KYC.

What Are Regulators Expecting?

In India, the Financial Intelligence Unit (FIU-IND) and RBI mandate the reporting of suspicious transactions under PMLA.

Banks and NBFCs are expected to:

- Maintain robust AML/CFT programs

- Submit Suspicious Transaction Reports (STRs)

- Conduct ongoing customer due diligence

- Implement automated monitoring systems with risk-based thresholds

Failure to comply can result in penalties, audits, and severe reputational loss.

Frequently Asked Questions (FAQs)

Q1: Are money mule accounts always opened knowingly?

No. Many mules are tricked into opening or sharing accounts via fake job offers or romance scams. Some are even offered commission to “help” with transactions.

Q2: What’s the legal implication for a money mule?

Even if unintentional, being part of a laundering scheme can lead to freezing of accounts, loss of funds, and in severe cases, criminal investigation.

Q3: How do criminals recruit money mules?

Common tactics include:

- Fake job offers promising high pay

- Online romance scams

- Phishing emails

- Social media “cash flipping” scams

Q4: Can banks detect mule accounts at the time of onboarding?

While it’s challenging, using enhanced KYC, employment verification (like eLockr), and digital footprint analysis can reduce the risk significantly.

Q5: How does OnGrid help in mule detection?

OnGrid helps verify:

- Identity authenticity

- Criminal background checks

- Employment history check

Leave a Reply