When you peel back the layers of India’s digital economy, you find a country that has reimagined how people prove who they are, how businesses build trust, and how regulators ensure everyone plays by the rules.

But behind this seamless ecosystem of instant loans, paperless onboarding, and friction-free payments lies a complex web of compliance frameworks — KYC, KYB, AML, FIU reporting, data privacy laws, and more. For API providers building the infrastructure of trust, understanding and adapting to these evolving regulations isn’t just a legal checkbox; it’s a fundamental part of product design.

This is a deep dive into India’s verification and compliance landscape — and what it really means to build responsibly in an age where data and trust are two sides of the same coin.

The Changing Nature of Digital Compliance in India

India’s regulatory journey is best described as a balance between innovation and vigilance. The country has witnessed an explosion of digital services — from instant credit to embedded finance — each relying heavily on identity and verification APIs.

But with every new innovation, regulators have stepped in to ensure the foundations of trust remain intact. Whether it’s a fintech onboarding a new customer, a bank verifying a business, or an NBFC preventing money laundering — compliance frameworks now sit at the heart of every API-driven operation.

In this evolving environment, KYC, KYB, and AML have become the three pillars of digital integrity — defining how individuals and organizations prove legitimacy, how transactions are monitored, and how risk is mitigated.

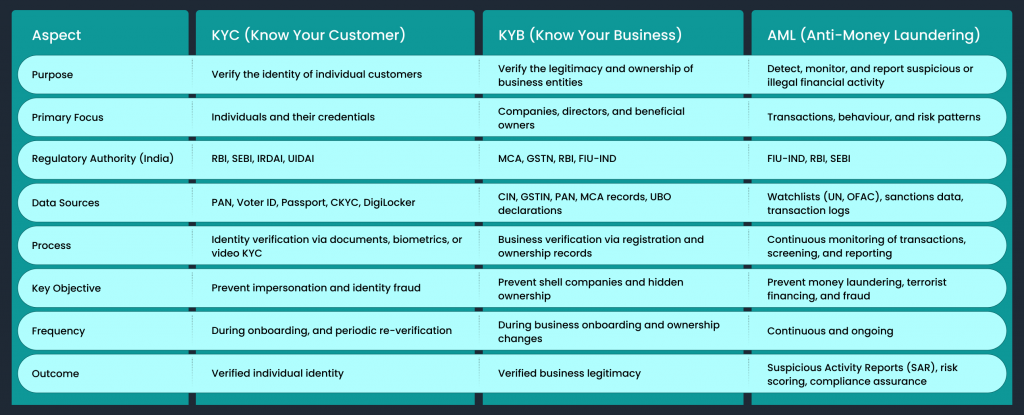

The Compliance Trifecta: KYC, KYB, and AML

Before we explore their nuances, here’s a quick comparative snapshot to understand how these three frameworks differ — yet complement each other in the larger regulatory ecosystem.

Understanding the Core of KYC: From Compliance to Confidence

At its core, KYC isn’t about forms and documents. It’s about confidence — knowing that the person behind a transaction is who they claim to be.

In India, KYC processes have gone through an incredible evolution:

- Traditional KYC – physical verification, paper-based proofs, and in-person validation.

- eKYC – National Id based digital verification, enabling instant authentication using UIDAI’s API.

- Video KYC – introduced under RBI and SEBI guidelines, allowing remote verification through live video calls.

Today, KYC APIs power everything from opening a bank account to verifying gig workers for delivery apps. But regulators have made it clear: automation can’t compromise privacy or consent. Every API transaction must adhere to purpose limitation, consent recording, and data minimization norms.

For API providers, this means designing for compliance from the ground up — encrypting personal data, limiting access, and maintaining tamper-proof audit trails.

“The real innovation isn’t in faster verification. It’s in verifications that build confidence without breaching privacy.”

KYB: The Unsung Hero of Compliance

While KYC has always been in the spotlight, KYB (Know Your Business) is quietly becoming just as critical.

As shell companies, money mules, and layered corporate structures become tools for financial crime, regulators are demanding deeper visibility into who owns and controls an entity.

In India, KYB goes beyond verifying the business registration number — it includes:

- Business identity validation (CIN, GSTIN, PAN).

- Director and beneficial owner verification through MCA records.

- Document verification (MoA, AoA, partnership deeds).

- UBO (Ultimate Beneficial Ownership) detection.

For B2B fintechs, payment gateways, and lending platforms, KYB is a non-negotiable. But for API providers, it’s also a challenge — how do you automate something so complex, where every business structure looks different?

The solution lies in data interoperability — connecting MCA, GSTN, NSDL, and bank data through APIs, while ensuring the process remains privacy-safe and auditable.

When done right, KYB doesn’t just prevent fraud — it helps fintechs onboard faster, build trust with regulators, and protect their ecosystem from reputational risks.

The AML Layer: Detecting Risk in Real-Time

If KYC and KYB are about identification, AML (Anti-Money Laundering) is about detection.

AML frameworks focus on monitoring transactions, identifying red flags, and reporting suspicious activity to the Financial Intelligence Unit (FIU-IND). In India, entities under RBI, SEBI, IRDAI, and PMLA are all expected to establish AML systems and follow strict reporting obligations.

For API providers, AML isn’t about transaction monitoring in isolation. It’s about embedding risk intelligence into every layer of onboarding and verification.

That includes:

- Screening against sanctions lists (UN, OFAC, domestic watchlists).

- PEP (Politically Exposed Persons) identification.

- Detecting synthetic or duplicate identities.

- Continuous monitoring for changes in user risk profiles.

This requires APIs that don’t just verify — they learn. AI models trained on behavioural and transactional data are becoming the new eyes of AML frameworks, spotting patterns that humans might miss.

“In the API era, AML isn’t a post-transaction process. It’s a pre-transaction intelligence system.”

The Data Privacy Revolution: Enter the DPDP Act

While verification and compliance keep systems secure, data privacy keeps them humane.

The Digital Personal Data Protection (DPDP) Act, enforced in 2024, has fundamentally reshaped how verification data is handled in India. It mandates:

- Explicit user consent for every data processing activity.

- Clear data retention limits and purpose boundaries.

- Strict cross-border data transfer conditions.

- Penalties for data misuse or unauthorized access.

For API providers, this isn’t just another compliance burden — it’s an opportunity to rebuild digital trust. Consent-led verification, granular data controls, and anonymized processing are now becoming product features, not afterthoughts.

Imagine a world where users can port their verified credentials across employers, banks, or platforms without repeatedly sharing sensitive documents. That’s where data portability and consent-driven frameworks will lead us.

RBI and SEBI’s Growing Influence on API Infrastructure

In India, financial regulators are no longer passive observers of fintech. They’re active architects of its digital foundations.

The RBI’s KYC Master Direction (amended frequently) now extends to entities using digital onboarding processes. It defines permissible modes of verification, including CKYC, DigiLocker.

Similarly, SEBI and IRDAI have framed digital onboarding standards for brokers, mutual funds, and insurance players. For API providers servicing these verticals, compliance with these sector-specific guidelines is essential.

The growing role of self-regulatory bodies (like Sahamati for Account Aggregators) also indicates that the future of compliance may be collaborative, not top-down. APIs will act as the connective tissue between regulated entities, consent managers, and data principals.

Challenges for API Providers in Navigating Compliance

Despite the clarity of regulations, practical challenges persist for those building in this space.

- Fragmented Data Sources

- Business and individual verification data lives across multiple registries — UIDAI, NSDL, MCA, GSTN, and more. Creating unified APIs without violating access rules requires careful orchestration.

- Business and individual verification data lives across multiple registries — UIDAI, NSDL, MCA, GSTN, and more. Creating unified APIs without violating access rules requires careful orchestration.

- Evolving Regulatory Guidance

- RBI’s digital KYC circulars, DPDP rules, and sector-specific mandates change frequently. Staying compliant is a continuous process, not a one-time implementation.

- RBI’s digital KYC circulars, DPDP rules, and sector-specific mandates change frequently. Staying compliant is a continuous process, not a one-time implementation.

- Data Security Expectations

- Encryption, tokenization, and anonymization are no longer optional. APIs are expected to demonstrate zero-trust architecture principles.

- Encryption, tokenization, and anonymization are no longer optional. APIs are expected to demonstrate zero-trust architecture principles.

- Balancing UX and Compliance

- Excessive friction can drive drop-offs; too little compliance can trigger penalties. The art lies in invisible verification — seamless yet compliant.

- Excessive friction can drive drop-offs; too little compliance can trigger penalties. The art lies in invisible verification — seamless yet compliant.

- Cross-Entity Coordination

- Fintechs, NBFCs, and verification providers often depend on each other’s APIs. This means shared liability and the need for transparent SLAs and audit trails.

Building Responsibly: What “Compliance by Design” Really Means

To survive and thrive in India’s regulatory maze, API providers need to internalize one mindset — compliance by design.

That means embedding legal and ethical considerations into every layer of product architecture:

- Consent-first architecture: Each verification starts with explicit, revocable user consent.

- Privacy-preserving data storage: Personal data is encrypted, masked, and deleted post-use.

- Granular access control: Different verification partners only see what they need to.

- Immutable audit logs: Every transaction can be traced, verified, and reported.

- Continuous monitoring: Real-time anomaly detection ensures compliance never sleeps.

When these principles guide development, compliance stops feeling like a constraint and starts becoming a differentiator.

Beyond KYC, KYB, and AML: The Next Frontier of Verification

The next decade of India’s digital economy will go beyond just verifying who someone is. It will focus on verifying what they do — employment, financial behaviour, reputation, and intent.

- Employment verification will become critical for gig platforms, MSME lenders, and staffing agencies.

- Credit-linked verification will blend traditional scores with verified work history.

- Behavioural verification — powered by AI and pattern recognition — will add a predictive layer to risk management.

For API providers, this signals a massive opportunity: to move from transactional checks to trust ecosystems, where verified data continuously flows between employers, lenders, and service providers.

“The future of compliance isn’t control — it’s collaboration. When data flows responsibly, trust compounds.”

The Road Ahead: Building for Trust, Not Just Regulation

Regulations will keep changing. Technologies will keep evolving. What will remain constant is the need for trust — the invisible currency that keeps India’s digital economy moving.

For API providers, the goal shouldn’t be just to comply with KYC, KYB, or AML guidelines. It should be to enable responsible growth — to help businesses onboard faster, consumers feel safer, and regulators stay confident that innovation doesn’t come at the cost of integrity.

Building in India’s compliance ecosystem is not easy. But it’s rewarding. Because each verified transaction isn’t just data validated — it’s trust reinforced.

Final Thoughts

Navigating India’s regulatory landscape requires patience, clarity, and empathy. It demands an understanding that every API call represents both a convenience and a responsibility.

The businesses that win will be those that see compliance not as a hurdle, but as an opportunity to build transparency into their DNA.

KYC, KYB, and AML are no longer isolated frameworks — they’re the grammar of trust in India’s digital economy. And those who master this language will define the future of verification.

Leave a Reply