Small and medium enterprises (SMEs) are the backbone of many economies, driving innovation, creating jobs, and fostering economic growth. However, accessing adequate financing remains one of the most significant challenges SMEs face. At the heart of SME lending lies the crucial process of underwriting—a systematic assessment of a borrower’s creditworthiness and risk profile. Effective underwriting ensures that lenders make informed decisions while enabling SMEs to access the financial support they need to thrive.

Let’s delve into the significance of underwriting in SME lending, explore the challenges involved, and highlight how technology is transforming this critical process.

The SME Lending Landscape

Why SMEs Struggle to Access Finance

Despite their pivotal role in the economy, SMEs often face barriers when seeking loans due to limited credit history, lack of collateral, and inconsistent cash flows. Traditional lenders, such as banks, are hesitant to provide loans without sufficient financial documentation, making it difficult for SMEs to secure funding through conventional means.

The Role of Alternative Lending

Fintech platforms, alternative lenders, and digital solutions are stepping in to bridge the gap by providing innovative financing options. These lenders leverage technology to streamline processes, reduce paperwork, and extend loans to SMEs previously excluded by traditional banking systems.

Yet, even with these advancements, underwriting remains a vital process to mitigate risk and ensure sustainable lending practices.

What is Underwriting in SME Lending?

Underwriting is the process by which lenders assess the viability of providing a loan to an SME. It involves evaluating the borrower’s financial history, operational performance, repayment capacity, and market risks.

In SME lending, underwriting is particularly complex due to:

- Limited financial documentation.

- Absence of formal credit scores.

- The diverse nature of SMEs, which range from sole proprietorships to mid-sized enterprises in varied industries.

Why Effective Underwriting is Critical

- Risk Mitigation: Proper underwriting minimizes the risk of defaults by ensuring that only creditworthy SMEs receive loans. This is crucial for maintaining a lender’s financial stability and reputation.

- Improved Loan Approvals: By adopting sophisticated underwriting processes, lenders can identify high-potential SMEs that might be overlooked due to traditional risk assessment models.

- Better Allocation of Resources: Accurate underwriting ensures that lenders allocate their resources to the right borrowers, maximizing returns and supporting economic growth.

- Enhanced Customer Trust: When underwriting is transparent and objective, it fosters trust between lenders and borrowers, encouraging long-term relationships.

Challenges in SME Underwriting

Despite its importance, underwriting in SME lending comes with several challenges:

1. Lack of Financial Data: Many SMEs operate informally, with incomplete financial records and limited documentation, making it difficult for lenders to assess their creditworthiness.

2. Variability Across Sectors: SMEs operate across diverse industries, each with its own dynamics and risk factors. Underwriting models must account for this variability to ensure accurate assessments.

3. Manual Processes – Traditional underwriting methods are often manual and time-consuming, leading to delays and inefficiencies.

4. High Costs – The cost of underwriting small-ticket loans for SMEs can be disproportionately high, making it less attractive for lenders to serve this segment.

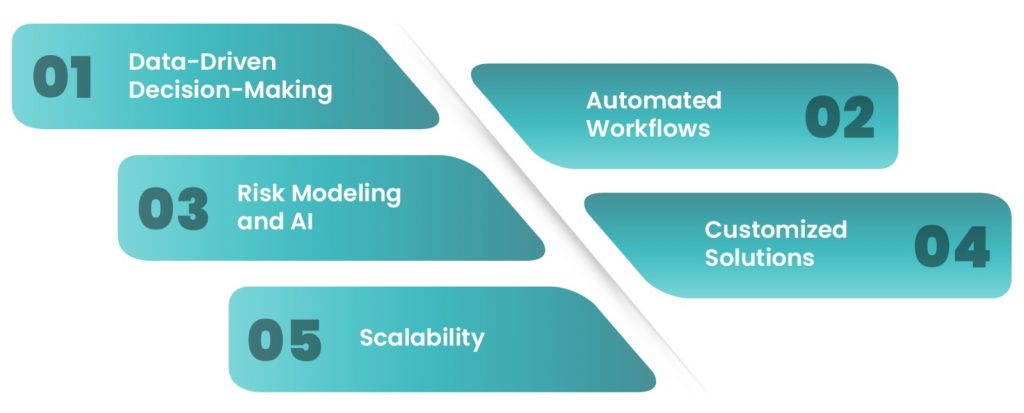

How Technology is Revolutionizing SME Underwriting

Modern technology is addressing these challenges by transforming underwriting processes into efficient, data-driven systems.

1. Data-Driven Decision-Making – Platforms leverage alternative data sources—such as GST filings, transaction histories, and social media activity—to create comprehensive credit profiles for SMEs. This allows lenders to assess creditworthiness even in the absence of traditional financial documentation.

2. Automated Workflows – By automating data collection, analysis, and scoring, digital platforms eliminate the inefficiencies of manual underwriting. This significantly reduces turnaround times for loan approvals.

3. Risk Modeling and AI –Advanced algorithms and machine learning models analyze vast datasets to predict risk with greater accuracy. These tools can identify patterns and anomalies that human analysts might miss, improving the quality of underwriting decisions.

4. Customized Solutions – Technology enables lenders to tailor their underwriting processes to specific industries or SME segments, accounting for unique risk factors and market conditions.

5. Scalability – Digital underwriting systems allow lenders to process a high volume of loan applications, making it feasible to serve the SME segment at scale.

Read Also: Minimize & Simplify Loan Cycle with Lending APIs

The Future of SME Lending

As the SME sector continues to grow, the demand for efficient and scalable lending solutions will only increase. Effective underwriting will remain a cornerstone of sustainable lending practices, but it will evolve in several ways:

1. Greater Adoption of Alternative Data – Lenders will increasingly rely on non-traditional data sources to evaluate SME creditworthiness, from e-commerce transaction data to utility payment records.

2. Deeper Collaboration Between Fintechs and Banks – Partnerships between platforms and traditional financial institutions will drive innovation and expand access to SME financing.

3. Regulatory Compliance and Transparency – With stricter regulations on lending practices, technology will play a crucial role in ensuring compliance while maintaining transparency in underwriting processes.

4. Focus on Sustainability – As ESG (Environmental, Social, and Governance) criteria gain prominence, underwriting models will incorporate sustainability metrics to align with broader societal goals.

Why Effective Underwriting Benefits SMEs

For SMEs, effective underwriting is not just about securing loans—it’s about building trust, credibility, and long-term financial stability. When lenders use sophisticated underwriting processes, SMEs can:

- Access tailored financing solutions.

- Benefit from fair and transparent lending practices.

- Build a robust credit profile for future growth.

Effective underwriting is the foundation of sustainable SME lending. It ensures that lenders can manage risk while empowering SMEs to unlock their full potential. By leveraging technology and adopting innovative approaches, platforms like Gridlines are transforming underwriting into a seamless, data-driven process that benefits both lenders and borrowers.

As the SME lending landscape evolves, effective underwriting will remain critical to bridging the financing gap and driving inclusive growth.

Leave a Reply