On a warm Monday morning, Ananya walked into her bank branch with a plan to open her very first savings account. She’d done her homework — compared interest rates, checked online reviews, and even shortlisted her preferred debit card design. But within minutes of sitting down, the bank officer smiled politely and asked the inevitable:

“Madam, please share your KYC documents.”

If you’ve ever opened an account, applied for a loan, taken out insurance, or even activated a new SIM card, you’ve been in Ananya’s shoes. KYC — or Know Your Customer — is one of those processes everyone has to go through, but few really understand. To most, it feels like a simple formality: submit a couple of IDs, sign a form, and you’re done. But beneath that routine lies a system that safeguards the very trust our financial world runs on.

What KYC Documents Actually Do

KYC documents aren’t just about ticking compliance boxes. They verify three simple but essential truths about you:

- Who you are — Your identity

- Where you are — Your address

- How you operate financially — Your income or financial status, in certain cases

Banks, fintech apps, insurers, stockbrokers, and even telecom companies rely on these documents to ensure they’re dealing with a legitimate customer — and to keep bad actors out of the system.

Why They Matter More Than You Think

Imagine giving a loan to someone without knowing their real name or where they live. Sounds absurd, right? Without KYC, that’s exactly the kind of risk financial institutions would be taking. These documents:

- Protect you from identity theft

- Help businesses follow laws laid down by RBI, SEBI, IRDAI, and others

- Build mutual trust between you and the service provider

Skipping or delaying KYC can mean locked accounts, frozen funds, or even cancelled services — not exactly the start you want with your bank or broker.

The Three Buckets of KYC Documents

Just like you carry different keys for your house, car, and office, KYC uses different documents for different purposes.

1. Proof of Identity (POI)

These say, “Yes, this is me,” and usually include your name, photo, and date of birth. Examples:

- Aadhaar Card

- Passport

- Voter ID

- PAN Card

- Driving Licence

Businesses use their own versions too — like incorporation certificates or GST registrations.

2. Proof of Address (POA)

These confirm your current address. Sometimes, the same document (like Aadhaar) can work as both POI and POA. Common examples:

- Utility bills (electricity, water, gas, phone) not older than 3 months

- Bank statements or passbooks

- Registered rent agreements

- Property tax receipts

3. Financial/Supporting Proofs

Needed for loans, credit cards, or high-value investments:

- Salary slips

- Income Tax Returns (ITR)

- Form 16

- Bank statements for the past 6–12 months

From Queues to Clicks: How KYC Has Changed

A few years ago, Ananya would’ve had to stand in line, fill out forms, attach photocopies, and wait days for verification. Today, thanks to digital onboarding, she can:

- Do eKYC — Verify instantly via Aadhaar OTP or biometrics

- Complete Video KYC — Show her documents to a compliance officer over a secure video call

- Rely on APIs — Businesses integrate systems that check documents directly with government databases

The time taken has dropped from days to minutes, and you no longer need to hunt for a photocopy shop.

The Small Mistakes That Cause Big Delays

Even with tech, many KYC requests still get rejected. Why?

- Using expired documents

- Uploading blurry scans

- Having name/address mismatches across IDs

- Submitting outdated proof of address

A quick double-check before hitting “submit” can save you a lot of frustration.

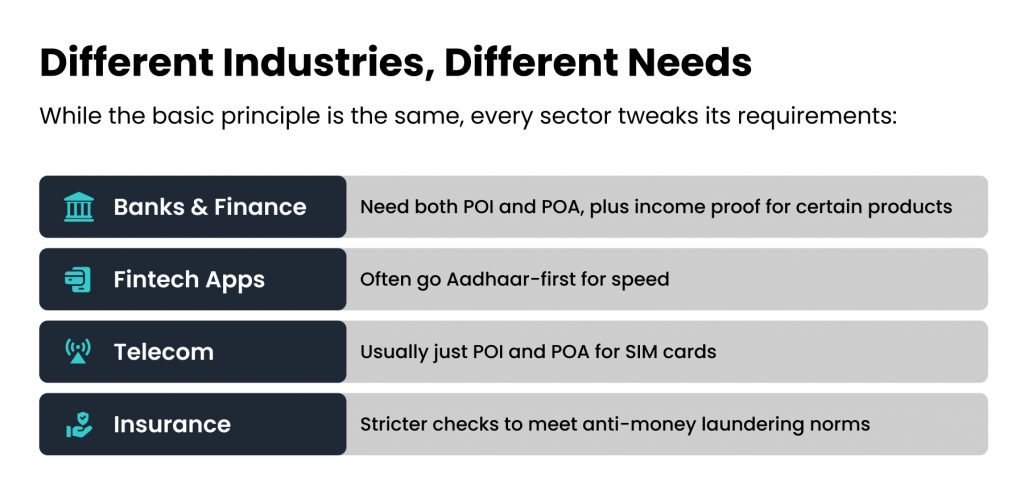

Different Industries, Different Needs

The Road Ahead

India is moving towards a future where you won’t have to carry or scan physical copies at all. DigiLocker, Aadhaar eSign, and account aggregators are already making consent-based, paperless verification the norm. Soon, you might just grant a one-time permission, and your verified details will be fetched securely from official records.

We’re also seeing a push for continuous KYC — where your records get updated periodically so they stay accurate, even if you move houses or change jobs.

KYC documents might seem like a small part of your customer journey, but they’re the invisible locks and keys that keep the financial system safe. They’re why your money reaches you securely, why fraudulent accounts get caught, and why the services you use can trust you from day one.

The next time you submit a KYC document, remember — you’re not just filling a requirement. You’re proving your authenticity in a system that depends on it. In a world where identities can be stolen with a click, those documents are your shield, your signature, and your access pass all rolled into one.

Leave a Reply