The Shape-Shifting Face of Cyber Fraud

Cybersecurity is no longer about passwords and firewalls. It’s about identity—knowing if the individual or organization on the other end of a digital interaction is real, trusted, and legitimated. In India, where financial inclusion, gig economy work, and digital-first onboarding have gone supernova, this question is no longer abstract. It is now existential for companies.

Nowadays, attackers don’t have to break into networks to wreak havoc; they can just slip in through the front door with a good imitation. Fake videos and forged identities are the newest additions to their arsenal. Phishing or malware can’t compare to these threats because they appear real, sound plausible, and pass manual checks with disquieting facility.

For financial institutions, fintech firms, HR companies, logistics firms, or capital markets firms, the risk couldn’t be greater. A single mis-clearance of a deepfake candidate, a counterfeit supplier, or a fake borrower can cause fraud loss, regulatory penalty, and reputational damage.

This is where APIs—real-time, automated, and evidence-based—enter the scene. Solutions such as Gridlines.io aren’t merely streamlining KYC (Know Your Customer), KYB (Know Your Business), and BGV (Background Verification). They are constructing the first line of defense against identity-driven cyber fraud.

What Makes Deepfakes and Synthetic IDs So Potentially Destructive?

The old fraud detection model was based on human intuition. A bank officer, an HR recruiter, or a vendor manager would look through papers, verify information, and “sense” legitimacy. That gut feeling worked as long as the scammers used Photoshop to forge papers or faked photocopies. The game changed though.

- Deepfakes: Artificially produced video and audio that impersonate real individuals with alarming verisimilitude. Consider a job applicant making a video KYC in which the face on the screen is that of an artificially generated person other than themselves. Human reviewers are easily tricked.

- Synthetic Identities: Not stolen identity, but made-up identities—a genuine PAN attached to an imitation Aadhaar, or a forged address with a genuine voter ID number. They clear superficial checks because some of the information is genuine.

- Size of the Threat: In 2024 alone, international fraud reports highlighted billions of dollars lost in synthetic identity frauds. Regulators such as RBI and SEBI in India are now encouraging institutions to implement layered, consent-based digital verification exactly to mitigate these risks.

What makes them so threatening is not merely their technology, but the way they undermine trust within digital environments. If companies can’t trust the identities they bring onboard, each transaction, partnership, or hire becomes a risk.

Why Manual Processes Are Failing

- Old onboarding and verification processes were designed for an age where fraudsters worked slowly. They weren’t designed to respond to AI-powered impersonation in large numbers.

- Time lag: Comprehensive Background checks or manual KYC takes days. Criminals use this window of opportunity to launch speedy attacks.

- Subjectivity: Human evaluators cannot identify subtle photo or video manipulations.

- Fragmented data: Without API integrations, teams have to deal with siloed databases and verification portals, leading to inaccuracies.

- User drop-offs: Complicated, paperwork-intensive workflows frustrate real users, resulting in high rates of abandonment. Ironically, fraudsters have more endurance than real customers.

The outcome? Companies are hit with a double whammy: legitimate users exiting because of friction, and fraudsters falling through the gaps.

The API Advantage: Real-Time Protection Against Cyber Fraud

Step in APIs. In an era where fraud adapts, defenses need to be real-time, elastic, and intel-driven. Gridlines.io delivers that via a set of plug-and-play verification APIs, which identify fraud indicators on the spot of interaction.

This is how APIs tip the scales:

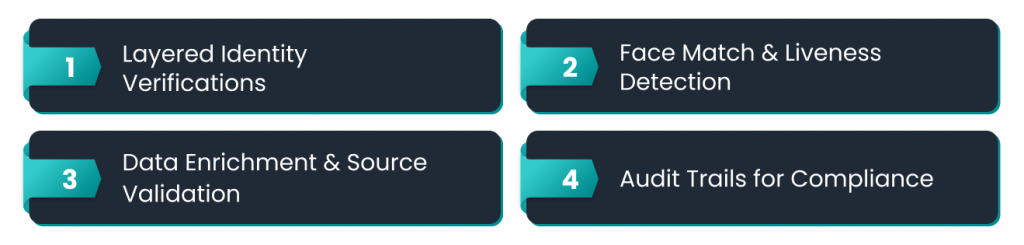

- Layered Identity Verifications

- Rather than checking against a single ID, APIs confirm multiple pieces of data at once—PAN, voter ID, driving license, bank account.

- Mismatches, anomalies, or outdated credentials are recognized immediately.

- This disrupts the “synthetic” cycle where fraudsters blend genuine and bogus information.

- Face Match & Liveness Detection

- AI-powered liveness verification ensures an actual person is shown, not a deepfake repeat.

- Face-match APIs match posted images to ID documents in milliseconds.

- Video morphing or AI overlays for fraudulent attempts can be recognized more accurately than human vision.

- Data Enrichment & Source Validation

- APIs retrieve regulated, source-driven data (e.g., CKYC, police records, court checks, bank verifications).

- By cross-verifying in official registries, synthetic identities get uncovered.

- Audit Trails for Compliance

- Timestamped verification records and automated logs enable organizations to remain compliant with RBI, DPDP, and SEBI rules.

- This eliminates the blind spot of manual processes when it comes to compliance.

Real-World Use Cases: Where the Threat is Hitting Hardest

The potential of deepfakes and synthetic IDs is not limited to any one industry. It transcends all industries where onboarding and verification are essential.

- Banking & Fintech: Synthetic ID loan applicants engage in fraudulent activities and contribute to NPAs (non-performing assets). PAN and bank verification APIs in real-time catch them early.

- Capital Markets: Investors onboarding with faked KYC credentials risk brokerages’ AML (anti-money laundering). APIs make CKYC fetches seamless so only authenticated identities enter.

- Logistics & Mobility: Delivery platforms are at risk of onboarding fake drivers with forged driving licenses. DL and RC validation APIs keep customers and brands safe.

- Employment & HR: Deepfake interviews and fabricated experience letters are increasing. Background verification APIs authenticate education, employment, and court documents in real time.

- Vendor & Partner Networks: Bogus suppliers siphon revenue through fake invoices. KYB APIs verify GST, ROC, and financial health, minimizing exposure.

Each of these instances highlights one fact: without API-driven real-time checks, manual verification isn’t sufficient.

Why APIs Are the Future of Cyber Fraud Defense

Cybersecurity is no longer about protecting systems—it’s about protecting trust. And trust starts with knowing with whom you are transacting. APIs enable that in a manner that is:

- Scalable: Onboarding 100 or 1 million users doesn’t faze APIs, and they never get tired.

- User-friendly: Faster onboarding journeys reduce drop-offs while increasing security.

- Evidence-backed: Every decision is tied to verified data sources.

- Proactive: Continuous monitoring shifts fraud detection from reactive to preventive.

In India, as the DPDP Act and RBI’s consent-driven KYC updates reshape compliance, businesses that rely on legacy manual methods risk falling behind. Those who embed APIs into their onboarding flows future-proof themselves—not just against cyber fraud, but against evolving regulations and user expectations.

Conclusion: Building a Fraud-Resilient Future

Deepfakes and synthetic identities are no longer edge-case threats; they are mainstream risks shaping the future of digital trust. For businesses, ignoring them is not an option.

But there’s good news: the same technology that enables fraud can also be used to stop it. With verification APIs like those from Gridlines.io, organizations can combine speed, security, and compliance in a single flow.

Defense against cyber fraud is not a firewall—it’s a ground of vetted trust, constructed API by API.

Leave a Reply