If you strip away the UI, the interest rate, the loan amount, the offers, the cashback, and the branding, every lending app—no matter how big or small—faces one core problem:

You don’t really know who is on the other side of the screen.

And in a business where identity equals risk, and risk equals money, this single uncertainty makes or breaks the economics of lending.

Over the last few years, India’s lending landscape has exploded. NBFCs, neobanks, payday apps, merchant lenders, BNPL platforms—everyone wants to issue credit fast. Borrowers want it even faster.

And so begins the real challenge:

How do you verify trust at high speed, high scale, and high accuracy… without letting fraud slip through?

This problem is so universal that even the most advanced lenders struggle with it.

The good news?

The solution already exists—and it’s becoming the default for serious fintechs: Video KYC.

Let’s dive into why the lending industry is converging on one truth:

Identity without real-time human presence is no longer verification—it’s guesswork.

The Lending Boom Created a Verification Crisis

For lending apps, onboarding is not a feature. It is risk architecture.

Every borrower you approve becomes a line in your future NPAs. Every borrower you reject becomes an increase in your CAC. Every fraudulent user you let in becomes a direct attack on your portfolio health.

Yet the speed race forced an uncomfortable compromise:

“Faster onboarding” often meant “weaker verification.”

Here’s what happened.

PAN verification didn’t prove the person holding the phone was the same person on the card.

Static data can be accessed, borrowed, or stolen.

Selfie matching became trivial to bypass with deepfakes, masks, and high-quality printed photos.

Telegram groups today openly circulate “selfie pass” kits.

Lending apps realized something alarming:

Thousands of “verified” users were not real verified users.

Identity was becoming increasingly digital, but fraud was becoming increasingly creative.

The gap kept widening—until Video KYC stepped in.

RBI Compliance Wasn’t the Reason Video KYC Became Mainstream. Fraud Was.

People often think Video KYC exploded because the RBI pushed for it.

Reality is slightly different.

Lenders were already drowning in:

- Synthetic identities

- Proxy onboarding

- Deepfake-based selfie attacks

- Loan stacking using the same face + different documents

- Borrower impersonation

- Mule accounts

- Repeat fraud rings

So, even before regulators nudged the industry toward better KYC, lenders themselves were searching for a verification process that brought presence back into digital identity.

Video KYC became the answer because it added one thing fraudsters constantly struggle with:

Real-time unpredictability.

You can fake documents.

You can fake selfies.

You can even fake a liveness blink.

You cannot fake real-time, two-way human interaction layered with AI checks.

Why Traditional KYC Fails Lending Apps

Let’s break down the exact gaps.

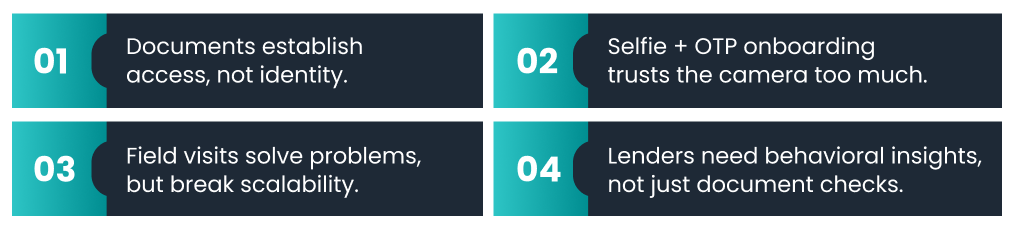

1. Documents establish access, not identity.

Anyone can obtain or buy an Aadhaar number or PAN.

Verification systems confirm if the document is valid—not if the person using it is the rightful owner.

2. Selfie + OTP onboarding trusts the camera too much.

Modern fraud tools allow:

- Real-time deepfake overlays

- Face swaps

- Video injection

- Pre-recorded clips

- Voice cloning

Trusting only the device camera is no longer safe.

3. Field visits solve problems, but break scalability.

Field verification methods are:

- Slow

- Expensive

- Dependent on manpower

- High drop-off

- Not suitable for pan-India digital lending

Video KYC replaces this with a real-time, remote, but still human-first approach.

4. Lenders need behavioral insights, not just document checks.

Verification is more than confirming an ID.

Lenders want to know:

- Is the borrower confident or coached?

- Is someone telling them what to say?

- Does the background match their declared address?

- Do their responses feel genuine?

- Are they trying to hide their face or surroundings?

APIs cannot detect these signals.

Real-time video can.

Video KYC Solves the Root Problem That All Lending Apps Share

The biggest challenge for digital lenders is not onboarding speed—it’s identity certainty.

Here’s how Video KYC solves that:

A. Prevents impersonation.

Liveness checks ensure the person is physically present—not a photo, not a deepfake.

B. Eliminates document manipulation.

Borrowers must show documents in the video, making edits and morphing obvious.

C. Captures intent.

Video interactions reveal behavioral red flags impossible to catch in static verification.

D. Brings the personal trust of a bank branch into a digital format.

Before digital banking, verification always involved a human.

Video KYC restores that.

E. Reduces drop-offs and accelerates approvals.

One call replaces paperwork, visits, and delays.

F. Provides stronger compliance and audit trails.

Recorded sessions create tamper-proof evidence.

G. Defeats fraud because fraud doesn’t like spontaneity.

If the fraudster can’t prepare for unpredictability, the attack fails.

Video KYC turns onboarding from a vulnerability into a defensive layer.

Lending Apps Without Video KYC Carry Higher Default Risk

The lenders with the highest NPAs almost always share these patterns:

- Reliance on document-only checks

- No real-time identity verification

- Weak liveness checks

- No background intelligence

- No behavioral analysis

- No dynamic identity confirmation

This leads to:

- Approving the wrong borrowers

- Approving synthetic profiles

- Approving people with zero repayment intent

- Approving fraudsters using the same face with multiple IDs

Video KYC is not just a compliance requirement—it’s a risk filter.

AI Has Turned Video KYC Into a Full Anti-Fraud Engine

Modern Video KYC is powered by multiple AI layers:

Face Liveness Detection

Confirms presence using micro-expressions, head movement, and texture analysis.

Deepfake Detection

Identifies face overlays, screen replays, and projection-based attacks.

Document Validation on Video

Matches video-seen documents with backend database checks.

Geo-Tagging

Makes region-based lending safer.

Background Intelligence

Detects green screens, virtual backgrounds, or suspicious environments.

Voice Pattern Analysis

Catches coached responses or hidden agents.

AI Cue Scoring

Helps lending teams auto-assess sessions.

This transforms Video KYC from a verification tool into a front-line risk engine.

Video KYC Increases Approvals—Counterintuitive but True

Lenders adopting Video KYC often report:

- Fewer manual reviews

- Faster verification

- Reduced onboarding drop-offs

- More borrower confidence

- Higher-quality data

- Better risk segmentation

Fraud reduces.

Approvals increase.

The portfolio improves.

Most teams assume Video KYC slows onboarding.

In reality, it just slows fraud.

Borrowers Prefer Video KYC Over Traditional Methods

In interviews and usability studies, borrowers call Video KYC:

- Convenient

- Faster than branch visits

- Less intimidating than paperwork

- More personal than a selfie KYC

- More trustworthy

There’s also a subtle psychological effect:

Borrowers tend to repay loans more responsibly when they’ve interacted with a human—even virtually.

The sense of accountability is higher.

Video KYC doesn’t just verify people.

It builds a relationship.

Conclusion

Every lending app eventually reaches the same realization: the biggest risk isn’t interest rates, borrower intent, or repayment capacity—it’s the uncertainty of not knowing who is actually behind the screen. Digital documents can be borrowed, identities can be stitched together, faces can be faked, and onboarding can be cleverly manipulated.

Over time, the industry has learned that static verification creates a blind spot big enough for fraud to slip through, especially when growth demands speed. Video KYC solves this by reintroducing real-time human presence into digital lending. It makes impersonation difficult, fraud risky, and onboarding transparent. Borrowers find it easy, lenders find it reliable, and regulators find it compliant. Most importantly, it bridges the gap between convenience and security—something digital lending has struggled with for years.

When identity verification becomes dynamic rather than static, lending becomes safer, smoother, and more predictable. That is the quiet but powerful shift Video KYC brings to the industry: not just as a compliance step, but as the most dependable way to ensure that the person borrowing money is truly who they claim to be. In a world where anyone can pretend to be anyone, this small layer of real presence becomes the foundation of trust.

Leave a Reply